Srpski / Arhiva brojeva / TREĆI BROJ / TOM MARKUSSEN: Regulation and competition in the telecommunications markets. Norway’s experience

Regulation and competition in the telecommunications markets. Norway’s experience

Tom Markussen

1. INTRODUCTION - BACKGROUND

What has happened in the Norwegian market for telecommunication following the liberalisation in the 1990s? This article deals with the sector-specific competition regulation in the telecommunications sector in Norway following the liberalisation in the 1990s. Here we first present developments in individual market segments up until today. After this we review current regulations in general, before turning special attention to how price controls are implemented. Finally we review developments and regulations in the mobile market in particular.

Up until the end of the 1980s, Norwegian Telecom (Televerket), which later changed its name to Telenor, had a monopoly on the provision of all telecommunications services in Norway. In 1988 its exclusive right to sell terminal equipment and internal telephone networks was abolished, with the remaining exclusive rights gradually done away with in the period from 1988 to 1998. In 1991 NetCom received a GSM licence, along with then Norwegian Telecom, thus breaking the monopoly on the provision of mobile telephony.

Norway is not a member of the European Union (EU). However, through the EEA Agreement, which governs trade and other economic matters between the EU and EFTA1 countries, EU regulation of the markets for electronic communication applies to Norway as well. For that reason, the liberalisation in Norway has taken place parallel to corresponding developments in the EU. Since the end of the 1980s the Commission and the national telecommunications authorities, such as the Norwegian Post and Telecommunications Authority (NPT)2, have facilitated increasing competition by means of rules and regulation at various levels. In 1998 the last exclusive rights were removed, thus liberalising the market for fixed network telephony, among others. The current regulatory package was approved by the EU in 2002, and the EU is currently preparing yet another revision of the regulations.

2. DEVELOPMENTS IN THE TELECOMS MARKET FOLLOWING DEREGULATION

Major changes have taken place in the Norwegian market for telecommunications after the liberalisation of the sector. Competition and liberalisation have led to the entry of several new operators, and Telenor’s market share has been reduced considerably. Retail prices have fallen in most product areas. However, Telenor continues to have a high market share and significant market power in a number of market segments. Moreover, there are only a limited number of operators with their own infrastructure, most of which are broadband providers. Most operators in the telecommunications market are pure-play service providers that resell services to end users and that need to purchase traffic capacity from network owners.

In this chapter we will take a brief look in trends in the number of customers, market share and prices in the retail markets for fixed network telephony, mobile telephony and broadband in Norway.3

2.1.Trends in the number of customers

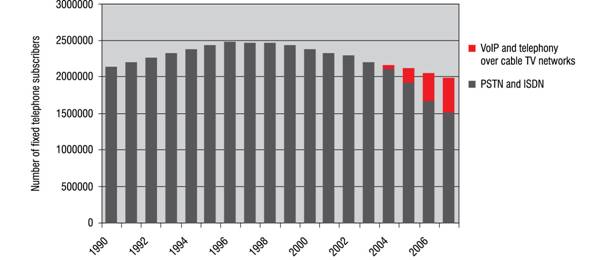

In Norway the number of customers with a fixed-network telephone has been dropping for many years. The peak in the number of customers was reached in 1996, when there were around 2.5 million subscribers. By the end of the first half of 2008 the number of customers had fallen to about 1.9 million. Even though in recent years there has been growth in the number of customers with voice over IP (VoIP), this growth could not make up for the total drop in the number of fixed-network customers. Figure 1 shows the trends in fixed network customers, including VoIP, from 1990 until 2007. By the end of the first half of 2008 the number of fixed-line telephony subscriptions corresponded to 73 % of all households.

Figure 1. Trends in the number of fixed network telephony subscriptions, including subscriptions for VoIP, in the period 1990-2007. Source: NPT’s telecom statistics

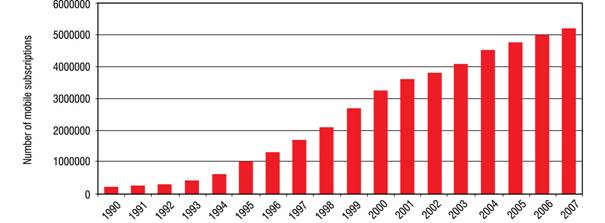

Figure 2 shows the growth in the number of mobile customers in Norway from 1990 to 2007. Today there are about 5.1 million mobile subscriptions (including pre-paid cards)4, and given Norway’s population of 4.8 million, this yields penetration of over 106 percent. When we correct for the fact that about 13 percent of the population has two or more subscriptions, it turns out that around 93 of 100 Norwegians have a mobile phone.

Figure 2 The trend in the number of mobile telephony subscriptions (including pre-paid cards) in the period 1990-2007. The figures in the period 1990-2004 include subscriptions in the Nordic Mobile Telephony (NMT) system. Source: NPT’s telecom statistics

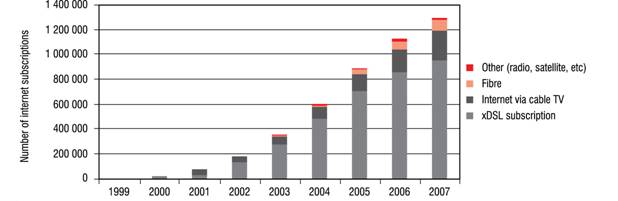

The number of broadband subscriptions has risen considerably in recent years. By the end of the first half of 2008, there were 1.375 million registered residential broadband subscriptions in Norway. It means that around 65 percent of households have broadband. Figure 3 shows the trend in the number of subscriptions from 1999 to 2007. The biggest share by far of broadband connections is based on xDSL technology.

Figure 3 The trend in the number of residential broadband subscriptions in the period 1999-2007. Source: NPT’s telecom statistics

2.2.Market share and number of providers

Telenor’s share of the market for fixed network telephony has been declining since the liberalisation in 1998. The former monopolist’s share of total revenues in the retail market for fixed network telephony was 68 percent in the first half of 2008. The next largest operator measured by total revenue was Tele2, with a 7.9 percent market share. These figures include VoIP. Telenor’s share of the total number of traffic minutes in the market for fixed network telephony was 60 percent in the first half of 2008. VoIP provider Telio was the next biggest when market share is calculated in terms of the number of minutes, with 9.1 percent of the total traffic volume. In Norway there were a total of 90 providers of fixed network telephony at the end of the first half of 2008, 81 of which offering VoIP.

At the end of the first half of 2008, Telenor had around 53 percent of the subscriptions in the Norwegian mobile market. The next largest mobile provider in Norway, NetCom, is owned by the Swedish company TeliaSonera, which also owns the reseller Chess. At the end of the first half of 2008 NetCom had a market share of about 20 percent, measured in the number of subscriptions, while Chess had 7.2 percent. At that time there were 27 mobile providers registered in Norway. Most of these were pure resellers. The growth of the mobile market is discussed in detail below.

In the broadband market Telenor had around 50 percent of the subscriptions at the end of the first half of 2008. Telenor’s market share has decreased in recent years. There were 157 broadband providers in Norway at the end of the first half of 2008, many of which offer broadband access only in local, limited geographic areas.

2.3.Price developments

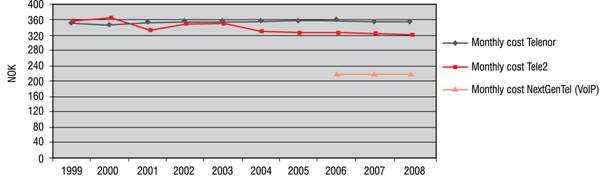

The nominal rates for traditional fixed-line telephony (PSTN/ISDN) have remained relatively stable during the past ten years. This can likely be explained in part by falling volume in the time period and by greater interest of consumers and providers in mobile telephony at the expense of fixed telephony. However, the introduction of VoIP has brought significantly lower rates to the consumers. The figure below shows monthly costs (usage and monthly charges) for a fixed-line (PSTN/ISDN) subscription of Telenor and Tele2 and a VoIP subscription of NextGenTel, given standard usage.

Figure 4 Monthly expenses (usage and monthly charges) for standard Telenor and Tele2 fixed network telephony subscriptions and a VoIP subscription from NextGenTel Source: Rate information gathered by NPT

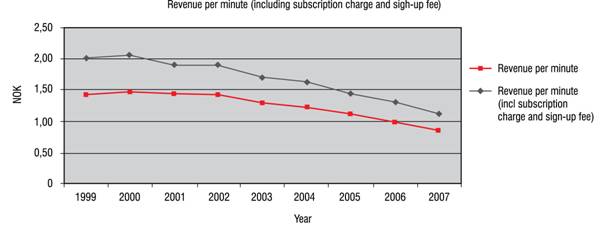

In recent years mobile telephony rates in Norway have fallen substantially, as illustrated by Figure 5. The figure below shows that mobile providers’ average revenues per minute (including subscription and sign-up fees) have fallen from approx. NOK 2 in 1999 to approx. NOK 1.1 by the end of 2007, which is a reduction of 45 percent. Retail prices in the mobile market also fell substantially in the period 1994 to 1999.

Figure 5 Revenues (excluding revenue from termination and roaming) per minute in the period 1999 – 2007. Source: NPT’s telecom statistics

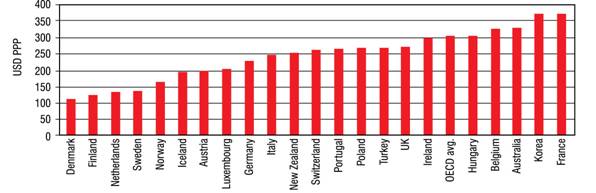

In OECD rankings based on statistics from Teligen, Norway is among the countries with the lowest retail prices for mobile telephony when disparities in purchasing power are corrected for. Figure 6 shows that in August 2008 Norway was the country with the fifth-lowest rates of average usage among the compared countries.5

Figure 6 Annual charges for mobile telephony for customers with average usage in OECD countries, including VAT and the OECD average in August 2008 in USD PPP, Source: Teligen

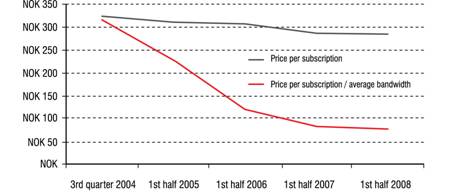

With regard to developments in retail prices for broadband connections, perhaps the most noticeable is that retail customers today receive substantially higher capacity for the same price that they paid a few years ago. For that reason one can say that the price per unit capacity has gone down considerably. Figure 6 illustrates this trend in the period third quarter of 2004 to the first half of 2008.

Figure 7 The trend in average price for broadband subscriptions and the ratio between average price and average bandwidth for broadband connection in the period third quarter 2004 to the first half of 2008. Source: Statistics Norway.

3. GENERAL INFORMATION ABOUT TELENOR

Telenor was established by the Norwegian state in 1855 as Telegrafverket (the State Telegraph Office). The company, which later changed its name to Televerket (Norwegian Telecom in English), was a state enterprise. In 1994 the company became a public limited company and one year later its name was changed to Telenor. In December 2000 Telenor’s shares were offered to the public. Today, the company is a partly-privatised6 limited company with independent business activities in the areas of mobile and fixed network telephony, broadband Internet and TV services via cable and satellite. Telenor is by far the largest provider of electronic communication services in Norway.

After its stock market debut in 2000, Telenor has expanded internationally, particularly in mobile telephony services. Through acquisitions and start-ups of own operations abroad, Telenor has obtained majority stakes in mobile companies in Denmark, Sweden, Ukraine, Hungary, Serbia, Montenegro, Thailand, Malaysia, Bangladesh and Pakistan. Telenor is also represented in the Russian mobile market through a minority holding in the mobile company Vimpelcom.

In terms of market capitalisation, Telenor is Norway’s second largest corporate group, valued at just over NOK 70 billion (around EUR 8 billion), as of February 2009. In all, Telenor has around 35,800 employees in 12 countries, approx. 11,000 of whom are in Norway.

4. SECTOR-SPECIFIC COMPETITION RULES

In 2002, the EU adopted six directives7, which comprise the current regulatory framework for the electronic communications sector. The primary purpose of this framework is enshrined in Article 8 of the Framework Directive, which sets forth the following objectives for the activities of the national regulatory authorities: 8

·Promoting competition

·Contributing to the development of the internal market

·Promoting the interests of the EU citizens

In 2003 the Commission identified 18 markets that could be relevant for the special, sector-specific competition regulation. The Framework Directive stipulates that markets that the Commission has predefined are to be analysed to determine whether they are characterised by effective competition or whether one or more undertakings has what is called “significant market power” (SMP). The providers designated as SMP operators are to have specific obligations imposed on them. The various possible remedies are obligations to provide access to networks and interconnection, establish accounting separation and publish reference offers, as well as price controls and obligations of “non-discrimination”. The obligations are intended to remedy competition problems in the relevant markets, such as denial to interconnect or excessive pricing, and are specifically justifiable in light of the objectives set forth in Article 8 of the Framework Directive. The obligations imposed will vary from market to market and among the specific instances. In the next Chapter we show how the price control obligations have been implemented in Norway. As competition becomes efficient in various markets, the sector-specific regulations are to be dismantled and replaced by general competition regulation.

By spring 2007 NPT had carried out the initial round of analyses of the 18 markets that the Commission had designated as relevant for sector-specific regulation in its first Recommendation. In 16 of the markets, NPT found that Telenor had significant market power. It is only in the wholesale market for international roaming on mobile networks (Market 17) and the market for broadcasting transmission services (Market 18) that NPT did not find that Telenor or others had significant market power. In the markets for voice call termination in individual fixed networks and mobile networks (Markets 9 and 16 pursuant to the 2003 Recommendation), NPT found that operators other than Telenor also had SMP.

In December 2007 the Commission adopted a revised list of relevant markets. The 18 markets from the original Recommendation have been reduced to seven in the new one. Among the markets removed from the revised Recommendation are the retail markets for traffic on fixed networks (Markets 3-6 in the old Recommendation) and the wholesale market for access to and origination on public mobile communications networks (Market 15). NPT has begun work to analyse the markets in accordance with the new Recommendation, including also assessing whether the sector-specific regulation in Norway, too, should be withdrawn from markets removed from the Recommendation on relevant markets.

5. IMPLEMENTATION OF PRICE CONTROLS IN NORWAY

Until the package of directives from 2002 was implemented in Norwegian law, most of the regulated telecoms services were subjected to obligations to charge cost-oriented rates. In practice this took the form of rate-of-return regulation9. The most important tool NPT had for monitoring compliance with this regulation,was product accounts prepared by Telenor each year, reviewed by an external auditor and submitted to the Authority. In addition, NPT required additional reporting for key wholesale products. An example of this is the forecasts that were prepared for interconnection on the fixed network in some years.

From 1995 until now, the principle of cost-orientation for Telenor’s services has largely been based on fully allocated historical costs. This means that Telenor has attributed its financial accounts’ operating expenses to various regulated product areas. The exception has been the costs related to LLU access (Local Loop Unbundling, access to Telenor’s copper-based access network). When Telenor launched its LLU product in spring 2000, Telenor had calculated the capital costs, which constitute the largest share of LLU costs, on the basis of the current cost principle10. In the case of LLU, the current cost principle resulted in rates that were higher than those that would have been obtained by applying the historical costs.

In most of the relevant markets that were defined by the Commission in 2003, NPT has issued decisions imposing price controls on wholesale products. For example, in all three markets for fixed network interconnection services (Markets 8, 9 and 10 in the 2003 Recommendation), price caps were set on the basis of fully allocated historical costs. Also in the LLU market (Market 11 in the 2003 Recommendation), NPT set a price cap on the basis of fully allocated historical costs, but also considered other factors, inter alia the incentives to invest in alternative access networks and the rates in other countries (benchmarking). In the market for wholesale terminating segments of leased lines (Market 13 in the 2003 Recommendation), an obligation has been imposed on Telenor to charge cost-oriented prices for wholesale leased lines up to and including 8 Mbit/s. Moreover, in the markets for access to the public telephone network at a fixed location (Markets 1 and 2 in the 2003 Recommendation) Telenor is obliged to offer wholesale line rental on the basis of a retail-minus model. For all these product areas, Telenor has been directed to implement a cost accounting system.

In 2005 NPT issued a decision in the markets for voice call termination in mobile networks (former Market 16). In the decision, a price cap regulation was imposed on the two largest mobile providers, Telenor and NetCom, based on a combination of fully allocated historical costs and benchmarking. Since this decision, NPT has developed an LRIC (Long-run Incremental Costs) model for determining the cost basis for termination in mobile networks. This model now serves as the basis for price controls. By 2010, NetCom and Telenor have been ordered to lower their rates stepwise towards a cost-oriented price calculated using LRIC.

In 2009 NPT will begin work to create an LRIC model for fixed networks. The model is intended to be used in the wholesale markets for call origination and termination in the public telephone network provided at a fixed location (Markets 2 and 3 in the new Recommendation) and possibly in the market for full and shared access to fixed access networks (LLU, Market 4).

In addition to price controls and cost accounting, NPT has also imposed on Telenor accounting separation obligations in several markets. Telenor has been directed to establish accounting separation in the wholesale market for broadband access (Market 12 in the old Recommendation), the wholesale markets for leased lines (Markets 13 and 14) and the market for access to and call origination in mobile networks (Market 15). Accounting separation, in combination with obligations on non-discrimination, are intended to prevent that operators depending on access to Telenor’s networks are subjected to a margin squeeze.

6. THE NORWEGIAN MOBILE MARKET IN DETAIL

Manual mobile telephony service was introduced in Norway in 1966 and was the precursor of the automatic Nordic Mobile Telephony (NMT) system established in 1981. Norwegian Telecom, later Telenor, enjoyed a monopoly on provision of mobile telephony until 1991, when GSM licences where awarded to Telenor and NetCom. Both operators introduced services based on GSM in 1993. For the remainder of the 1990s, there were only these two providers in the Norwegian mobile market. Telenor and NetCom rolled out good coverage nationwide, and the market grew sharply in the number of customers. Starting in 2000, Telenor and NetCom gave resellers access to their networks. In 2003, Tele2 became the first MVNO11 in Norway, with an agreement to use Telenor’s mobile network. Since then more MVNOs were established and there are now four MVNOs in the Norwegian market.

In 2000, both NetCom and Telenor were awarded UMTS licences following a beauty contest. A further two licences were also awarded, but Tele2 eventually returned its licence. The last company that had received a licence went bankrupt before it could begin to build a network. The company Hi3G was awarded one of these unused licences in 2003, but the company has not yet begun to roll out the network. Although according to its licence, at least 30 percent of the residences in the country are to be covered by September 2009, Hi3G has recently applied for a 30 month postponement of the obligation to comply with this requirement.

In 2005, Network Norway received a GSM 900 licence and opened its own mobile network in 2007. Network Norway has concluded a national roaming agreement with Telenor. Tele2 is currently an MVNO on NetCom’s network. Network Norway and Tele2 have teamed up to form a joint infrastructure company, Mobile Norway, which was awarded Norway’s fourth UMTS licence in December 2007. The new company has begun to roll out mobile networks in many of the largest cities in Norway. Together, Network Norway and Tele2 had around 15 percent of the customers in the retail market at the end of the first half of 2008.

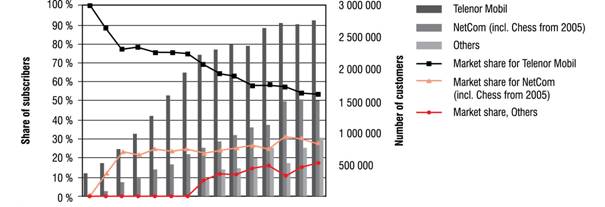

All told, there are just under 30 registered mobile telephony providers in the Norwegian market. In addition to the companies with their own spectrum licences, there are, as has been mentioned, a number of resellers and MVNOs. Figure 8 below shows changes from 1993 to the present in customer volume and market share in the retail market for Telenor, NetCom and “others”, i.e. independent resellers and MVNOs in Norway. It is evident that Telenor was losing market share over the entire period, though it is still clearly the largest operator.

Figure 8 Telenor, NetCom and other operators’ subscription volume and market shares in the retail market in period 1993-2007. Source: NPT’s telecom statistics

Both Telenor’s and NetCom’s mobile networks have excellent coverage. For example, Telenor’s GSM network currently covers 99.8 percent of the Norwegian population and 85.2 percent of the land area12. Since 2007, Telenor has upgraded its network with HSDPA, and this technology now reaches 86 percent of the population.13

As shown above, the retail prices in the mobile market have fallen considerably in Norway in the 2000s, especially after 2002. In addition to competition between Telenor and NetCom, there are several factors that have likely contributed to this price decline. Three probable causes of this price decline are the following:

·Number portability. Starting in December 2001 it has been possible to keep one’s mobile number when switching mobile operators. Since that time more than 3.5 million subscribers have kept their mobile number when switching operators. Number portability has helped to reduce the costs of switching and boosted competition in the Norwegian mobile market.

·The existence of resellers and MVNOs. It is largely resellers and MVNOs that have been the price leaders in the Norwegian mobile market. In the period 2001-2005 NPT actively monitored the market to ensure that resellers obtained adequate terms for access to the mobile networks, and in 2002 NPT issued a decision reducing the charges that resellers had to pay for access to Telenor’s network. Tele2 concluded an agreement for MVNO access from 2003, and in recent years they have enjoyed great success and have been at the forefront in lowering prices. The independent operators currently have a market share of about 20 percent (cf. also Figure 8)

·The rate comparison service Telepriser.no. The Norwegian Post and Telecommunications Authority has since August 2002 operated the website www.telepriser.no, where consumers can compare the rates offered by the various service providers for fixed telephony, mobile telephony, VoIP and Internet. This service has been a huge success, and the small mobile providers have often fought to be at the top of the rankings with the lowest rates.

6.1.Current regulation of the Norwegian mobile market

Until recently, however, Norway has been one of the few countries in Europe with only two mobile networks. Most European countries have three or four. Over the past 15 years Telenor and NetCom have built mobile networks with good coverage throughout the country, and by themselves have benefitted from the large number of customers and heavy traffic in their networks. A duopoly like this one increases the risk of poorly functioning competition. For that reason, in line with the purpose of sector-specific regulation, NPT wishes to facilitate the rollout of new mobile networks. That is why the sector-specific regulation has been aimed at rolling out more networks.

In 2006 NPT found that Telenor had significant market power in the market for access and origination in mobile communications networks (Market 15 in the 2003 Recommendation). At that time, Telenor had a market share of over 60 percent. Consequently, NPT imposed specific obligations on Telenor, including directing the company to provide access to national roaming and MVNOs. The Commission has now removed this market from the revised Recommendation. NPT has begun to assess whether there are special circumstances in the Norwegian market that, in view of the competitive situation, still necessitate regulation.

The regulation of mobile termination charges has also been aimed at bringing about better infrastructure competition. In the course of the last 8-10 years, mobile termination charges have gradually been reduced, initially the most by Telenor, though later also substantially by NetCom as well. Until 2007, NPT regulated Telenor’s and NetCom’s termination charges on the basis of cost accounts based on fully allocated historical costs. After the development of an LRIC model, Telenor and NetCom now have identical termination charges, and from 2010 their charges are to be cost-oriented, calculated using the LRIC model.

According to a decision by NPT from November 2008, new entrants in the mobile market, i.e. Network Norway, Tele2 and the other MVNOs, are also to reduce their termination charges substantially over a two-year period. However, these operators are permitted to have charges that are about 50 percent higher than those of Telenor and Netcom in 2010. The reason for time-limited asymmetry between the new and the established operators is the objective of giving the new operators better opportunities to build up customer bases and roll out their own mobile networks.

NPT has now begun to revise the LRIC model for mobile termination, among other reasons, to include 3G technology. The new model will probably also calculate the costs for new operators, so that it can be applied to regulating them also in the period after 2010.

Both the access regulation in former Market 15 and the regulation of mobile termination charges (Market 16) have as their objectives investment in more mobile networks in Norway, stronger competition and lower retail prices. These are intrusive remedies and in the long run some of them will likely be unusable in regulating the market. In the previous section, it was commented that number portability and the rate comparison service Telepriser.no are probable reasons for stronger competition and lower rates in the mobile market in recent years. Both of these measures are examples of less intrusive remedy use, which can reduce the cost of switching or make more market information available to consumers. The use of such remedies can facilitate better competition without a more direct regulation. This is in line with NPT’s strategy of allowing market forces to work by themselves where they are expected to yield results as good as or better than regulatory remedies.

7. SUMMARY - CONCLUSIONS

There have been profound changes in the Norwegian telecommunications market following the liberalisation in the 1990s. The incumbent, Telenor, has lost market share to new operators in all market segments. This has taken place in parallel with the explosive growth of mobile telephony, partly at the expense of fixed telephony, and the broadband market has also mushroomed. Competition has resulted in lower retail prices, a broader array of services and better network coverage. However, Telenor continues to dominate a number of market segments in Norway, and it is likely that sector-specific regulation will be necessary in many areas for a long time to come.

The Norwegian Post and Telecommunications Authority has a strategy of minimal regulation. This means, for example, that NPT wants market forces to work where they are expected to yield results as good as or better than direct regulation. It is also NPT’s experience that it is important to have clear regulatory goals, in line with the EU regulations, and to tailor and target remedies to reach these goals. This means, for example, that if it is possible to bring about competition between parallel networks in a market, the regulation ought to attach importance to this.

With regard to price controls in Norway, there has been a change following the implementation of the EU regulatory package from 2002. NPT has attached greater importance to reducing the degree of asymmetric information between the regulated operators and the Authority, regulating prices so as to give greater incentives to investment and efficient production and ensuring a long-term perspective and improved predictability in its regulation. For that reason, in several markets, NPT has moved away from rate-of-return regulation and has employed price caps. There is also a movement away from regulation based on fully allocated historical costs and towards the use of LRIC models. This is in line with the developments in a number of other European countries.

1 The European Free Trade Association (EFTA) was formed in 1960 as an alternative to the European Economic Community (today the EU). To this day, Norway, Switzerland, Iceland and Liechtenstein are EFTA members, though Switzerland does not participate in the EEA Agreement.

2 NPT is an independent administrative agency under the Ministry of Transport and Communications. NPT was formed in 1987. The agency’s principal area of responsibility is to regulate and oversee the postal and telecommunication sectors in Norway.

3 The source for the figures in this chapter and the remainder of the article is NPT’s telecom statistics and price information obtained by NPT, unless otherwise explicitly mentioned.

4The numbers in Figure 2 to are not adjusted to take account of subscriptions used for machine-to-machine communications. For the estimate of 5.1 million subscriptions at the end of 1st half of 2008 such an adjustment has been made.

5Figure 6 shows a comparison of expenses for mobile telephony in various OECD countries for consumers with average usage. The comparison is based on an OECD basket intended to represent given mobile phone use, with a certain number of calls/call minutes to domestic fixed networks, to mobile telephones and to international numbers. In the comparison the price for this combination of number of calls and minutes is given in US dollars, corrected for differences in purchasing power, or USD PPP. The average for the OECD is calculated as an unweighted average for the countries included in the comparison. In the OECD statistics comparisons were made of expenses for mobile telephony for three different usage groups: Low usage, average usage and high usage. Here NPT has only included the figure for the category average usage. In the comparison for February 2008 Norway was ranked fourth for low usage and seventh for high usage.

6The Norwegian Government currently has the ownership of 53.97 % in Telenor.

7 The six directives are: Framework Directive (Directive 2002/21/EC), Access Directive (Directive 2002/19/EC), Authorisation Directive (Directive 2002/20/EC ), USO Directive (Directive 2002/22/EC), Privacy and Electronic Communications Directive (Directive 2002/58/EC) and Directive on competition in the markets for electronic communications networks and services (Directive 2002/77/EC).

8 Article 8 (2), (3) and (4) of the Framework Directive.

9 In this context “rate-of-return regulation” means that rates are to be set so as to enable the regulated company to earn a reasonable rate of return on capital employed and no more.

10 In this case, assumed existing network structure.

11A Mobile Virtual Network Operator (MVNO) is a mobile operator which does not have its own radio network but concludes agreements with an operator that owns its own mobile network for access to the radio portion of that network. An MVNO has its own core network, switch networks and related support systems as well as its own mobile network code (MNC). A reseller, on the other hand, does not provide its own traffic production, but purchases all traffic production from the network operator.

12 Norway’s total area is 384,802 km2 (including Svalbard). The area of the main land of Norway is 323,782 km2.

13Source: www.telenor.no

Author

Tom Markussen obtained his cand.oecon.degree at the University of Oslo in 1997. He has been working in the Norwegian Post and Telecommunications Authority since 2001, both as an economic adviser and head of the Section of Market Surveillance. He has been closely involved in the Authority’s general work on markets analysis and regulation, and more specifically conducted analysis and imposed remedies in the mobile markets. Markussen has also contributed in other regulatory fields within the scope of the Authority.